Economists often talk about “laws” in economics. Two of the most basic ‘laws” are the law of supply and the law of demand. Nearly every economic event results from the interaction of these two laws. The law of supply says that the quantity of a good supplied (i.e., the amount owners or producers offer for sale) rises as the market price rises, and falls as the price falls. Economists do not really have a “law” of supply, though they talk and write as though they do.

An important function of markets is to find “equilibrium” prices. These are prices that balance the supplies of and demands for goods and services.

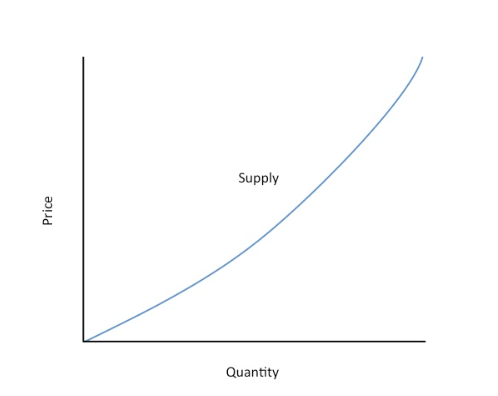

Economists often talk of “supply curves.” A supply curve traces the quantity of a good that sellers will produce at various prices. As the price falls, so does the number of units supplied. Equilibrium is the point at which the demand and supply curves intersect–a single price at which the quantity demanded matches the quantity supplied.

Why does the quantity supplied rise as the price rises and fall as the price falls? There are some good reasons. First, consider the case of a company that makes a consumer product. Acting rationally, the company will logically buy the lowest cost materials for a given level of quality. As production (supply) increases, the company has to buy progressively more expensive (i.e., less efficient) materials or labor, and its costs increase. It charges a higher price to offset its rising unit costs.

——-

This Micro Brief is part of an ongoing series provided as a general public information service. These concepts underpin modern economic analysis. Find out more about smarter capital investment decisions using economics at www.lyttonadvisory.com.au.